Published on ILMI Initiative | June 2026

📑 Quick Navigation

In July 2023, Beijing quietly turned two obscure metals into geopolitical weapons. Gallium and germanium—the elements that make high‑frequency chips and fiber optic cables possible—became subject to export controls that required Chinese government approval. Within months, gallium exports from China collapsed by nearly 70 percent. Three US defense contractors later disclosed they held less than 90 days of inventory for key semiconductor materials. The disclosure was classified. The fact it happened was not.

A year later, an AI supply chain model at a European battery manufacturer flagged something equally disturbing. Over 70 percent of the world’s cobalt refining capacity sat inside China. The cobalt came from the Democratic Republic of Congo, but the furnaces that turned ore into battery‑grade cathode powder were concentrated in a single country. The report landed in a procurement manager’s inbox. It sat unread until the next crisis hit.

This is the new resilience blind spot: Not the chokepoint you see on a shipping map. The one hiding inside your supplier’s supplier, buried in a processing facility nobody thought to audit.

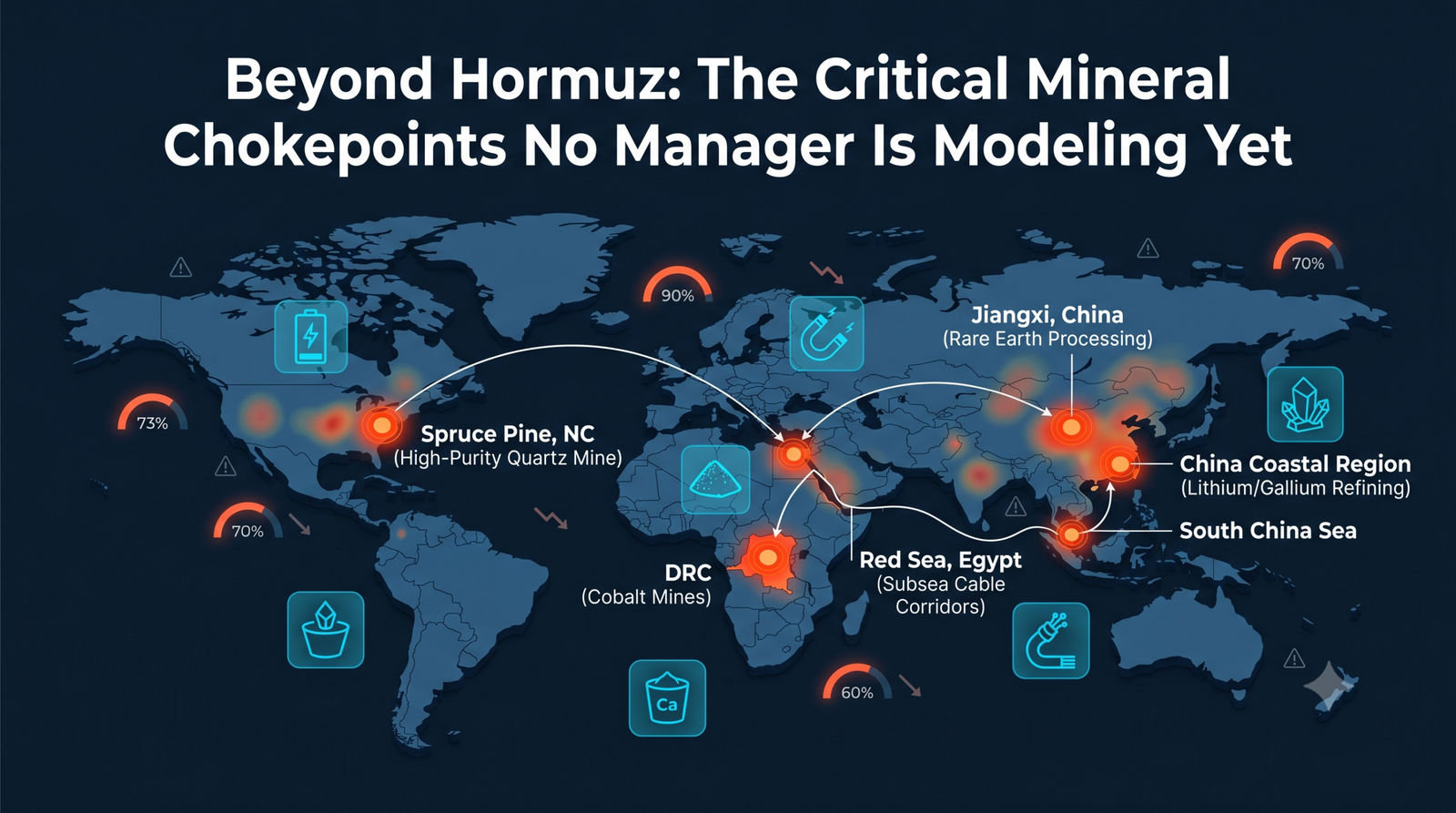

The Next Hormuz Won’t Be a Strait

Everyone watches the Strait of Hormuz. Tanker traffic, naval posturing, insurance premiums. That anxiety is already priced into markets and boardroom conversations. The sharper question, the one that forums and risk committees are finally starting to ask, is this: if not Hormuz, then what? What is the next single point of failure that nobody is talking about?

The answer is not another oil route. It is:

- A factory in China’s Jiangxi province that processes almost all the world’s heavy rare earth elements

- A quartz mine in Spruce Pine, North Carolina—a town most executives couldn’t place on a map

- A cable landing station in Egypt where a single dredging accident could slow internet traffic across three continents

AI can already see these vulnerabilities. Platforms like Resilinc’s AI risk monitoring and the UVA Biocomplexity Institute’s supply chain mapping tools flag concentrated dependencies in near real‑time. The algorithms that monitor your supply chain are sending these alerts right now. But most corporate risk models still categorize geopolitical disruption as a single line item. Legal, procurement, and strategy don’t talk to each other. So the warning sits in an unread email while the world hurtles toward the next outage.

Six Critical Nodes That Control Every GPU, Every EV Battery, Every AI Data Center

The AI race gets framed as a software competition. Benchmarks. Parameter counts. Training runs that cost $100 million. But underneath every transformer block humming inside a data center is a physical supply chain that begins in a mine. That supply chain has six deep bottlenecks. Most are controlled, to an uncomfortable degree, by a single country.

Rare Earth Processing (China)

Gallium Production (China)

Cobalt Mining (DRC)

Quartz Crucibles (1 Mine)

Rare Earth Processing

China processes over 90 percent of all rare earth elements globally (IEA, 2025). The mines themselves are distributed across Australia, the United States, Myanmar, and Russia. But China spent 30 years building the processing infrastructure while Western nations outsourced it. The result is a master single‑point failure.

Rare earths are irreplaceable in the permanent magnets inside every electric motor, every wind turbine, and the precision actuators used in semiconductor manufacturing equipment. If China restricts processing, the green energy transition and the AI chip supply chain both hit a wall simultaneously.

Gallium and Germanium

China produces roughly 80 percent of global gallium and 60 percent of germanium. The July 2023 export controls were not a warning shot. They were the opening salvo.

Gallium arsenide and gallium nitride are foundational to the high‑frequency chips used in 5G infrastructure, radar systems, and satellite communications. Germanium is the substrate in the fiber optic cables that carry 97 percent of the world’s intercontinental data traffic. When Chinese gallium exports fell by nearly three‑quarters, supply chain managers in the defense and telecom sectors discovered they had no plan B.

Cobalt

The Democratic Republic of Congo produces 73 percent of the world’s mined cobalt. But mining is only half the story. Roughly 70 percent of global cobalt refining capacity sits in China, much of it controlled by companies like CATL and Huayou Cobalt.

Cobalt is the cathode material in lithium‑ion batteries that power data center UPS systems—the backup power keeping AI inference running during grid fluctuations. A disruption in either Congolese mining or Chinese refining cascades directly into the reliability of the digital infrastructure that underpins global finance.

High‑Purity Quartz

This is the bottleneck almost nobody talks about. NVIDIA’s H100 and B200 GPUs require quartz crucibles to grow the silicon ingots that become chips. The only commercially viable source of ultra‑high‑purity quartz is a single mining and processing operation in Spruce Pine, North Carolina, operated by Sibelco.

Roughly 90 percent of the semiconductor‑grade quartz crucibles used worldwide trace back to that one mountain town. When Hurricane Helene flooded the Spruce Pine facility in September 2024, the global chip industry held its breath. Production eventually resumed, but the episode exposed a vulnerability that no amount of fab investment in Arizona or Taiwan can fix.

Subsea Cable Corridors

Roughly 1.7 million kilometers of submarine cables carry 97 percent of intercontinental data traffic. The Red Sea corridor is one of the most critical. Through that narrow passage moves over 20 percent of global internet traffic and up to 95 percent of the data exchanged between Asia and Europe.

Egypt alone hosts 10 cable landing stations, five on the Mediterranean and five on the Red Sea. In early 2024, Houthi attacks in the region damaged multiple cables. Repairs in contested waters took months, with one operation stretching close to six months. The financial systems, cloud services, and AI model training runs that depend on those cables had to reroute through longer, more expensive paths. Not every firm had tested its failover procedures.

Lithium Refining

The Lithium Triangle—Chile, Argentina, Bolivia—holds 58 percent of the world’s proven reserves. But China dominates the chemical processing that turns raw lithium carbonate into battery‑grade lithium hydroxide. Over 60 percent of global lithium refining happens in China.

JP Morgan’s 2026 commodity forecast projects lithium demand growing 16 percent year over year, driven by data center battery storage expansion and EV fleet growth. A refining disruption in China does not just raise prices. It idles battery factories on three continents simultaneously.

The Chokepoint Override Protocol: A Three‑Step Framework for Managers

You do not need to become a geologist or a trade negotiator. You need a protocol that forces your organization to act on warnings that are already sitting in your systems. Here is the Chokepoint Override Protocol.

Audit What Your AI Tools Actually Flag

Your supply chain analytics platform is already identifying critical nodes. Most companies ignore these alerts because they do not fit neatly into existing risk taxonomies. Pull the reports. Look for single points of failure where more than 50 percent of a critical material passes through one facility, one port, or one country. These are your concentration risks. Write them down. Circulate the list. Make the invisible visible.

War‑Game the Top Three Nodes

Take the three nodes your AI rates as most critical. Run the failure scenario:

- What happens if Chinese gallium exports stop for 60 days?

- What happens if the Red Sea cable corridor goes dark for 90 days?

- What happens if the Spruce Pine quartz mine floods again and stays offline for half a year?

Tesla halted most production at its Berlin factory for two weeks starting in late January 2024 because Red Sea shipping disruptions delayed critical components. That was not a mineral embargo. That was logistics friction on a single route. Now imagine that same duration of disruption hitting a material you cannot substitute and a supplier you cannot bypass. The war game will surface dependencies your org chart does not see.

Pre‑Authorize Budget and Decision Pathways

When the alert hits, you will not have time for committee approval while the port is already closed. Establish pre‑authorized budget and decision rights for chokepoint disruption. This is emergency procurement authority that bypasses normal approval chains. The board signs off on the framework in advance, not during the panic.

Japan learned this lesson the hard way after China’s 2010 rare earth embargo. Japan now maintains strategic reserves equivalent to 60 days of consumption for 31 critical minerals, managed by JOGMEC. That is not a stockpile. That is an institutionalized override.

The Forward‑Looking Warning

In February 2026, the US Department of Energy announced $500 million for domestic critical mineral production, targeting geothermal lithium brine extraction, rare earth recovery from coal byproducts, and germanium from coal ash. These are engineering‑ready processes, not lab experiments. But the rare earth processing gap will not close by 2030. It took China 30 years to build the metallurgical expertise, the chemical separation plants, and the environmental remediation capacity. The United States is not going to replicate that in four years, no matter how much money is allocated.

Japan’s strategy after 2010 was tripartite: diversify supply sources, develop substitutes, create stockpiles. Toyota’s research division produced permanent magnets with 50 percent less rare earth content by optimizing grain boundary engineering. Those magnets are not as strong as neodymium‑iron‑boron. They are good enough for many applications. And good enough breaks monopoly leverage.

The United States remains a decade behind this approach. The Inflation Reduction Act’s domestic content requirements for EV batteries are a start, but there is no equivalent program for semiconductor‑grade minerals. No stockpile mandate for gallium. No substitution research program for the quartz that grows silicon ingots.

The Strait of Malacca still carries around 40 percent of global maritime trade in 2026. It remains one of the world’s most critical physical chokepoints. But the next crisis will not come from a tanker blockade. It will come from a factory shutdown, a cable cut, a processing facility that nobody thought to diversify because no single department owned the risk.

The fragile system beneath the internet and the energy transition is not failing easily. It is degrading under pressure, and staying degraded. A single flooded mine or a single severed cable can quietly reshape whole industries while most managers still think the real danger lies in a map of the Middle East.

Will Your Organization Listen When AI Warns You?

The next Hormuz will not be a strait. It will be a single factory. A single cable ship. A single data center. AI will see it coming. The models are already flagging the concentrations. The question is whether your organization has built the institutional muscle to act on those warnings before the crisis hits—or whether the report will sit in an inbox until the lights flicker and the supply chain breaks.

Globalization, at least the version that assumed frictionless trade, is over. The French are worried about French supply chains. The Germans are worried about German supply chains. What was once a coordinated Western approach is fragmenting into a free‑for‑all. Critical minerals are now dictating diplomatic alignments, not just commercial contracts.

Every AI capability roadmap should have a mineral dependency analysis attached to it. Almost none of them do. That is the gap between where the industry thinks the risk lives and where the risk actually lives. So ask yourself now: how many organizations will wait until their own Spruce Pine moment to ask why AI’s warnings went unheeded?

And right now, the rocks have very few owners.

This article continues the exploration of the Resilience Blind Spot—the gap between what AI predicts and what human institutions dare to act upon. For the foundational framework, see the Predictability Paradox. For the energy‑sector application that preceded this analysis, see the Hormuz crisis deep‑dive.

Published by ILMI Initiative (International Liquidity and Market Intelligence Initiative) | Research on global market risks and supply chain vulnerabilities

@media (max-width: 600px) {

/* Stack stat cards vertically */

div[style*=”grid-template-columns: repeat(2, 1fr)”] {

grid-template-columns: 1fr !important;

}

/* Reduce hero padding */

div[style*=”padding: 30px 15px 40px 15px”] {

padding: 25px 12px 35px 12px !important;

}

/* Make Quick Navigation non-sticky and smaller */

div[style*=”position: sticky”] {

position: static !important;

margin-top: 20px !important;

padding: 16px !important;

}

div[style*=”position: sticky”] a {

font-size: 0.85rem !important;

}

div[style*=”position: sticky”] span[style*=”border-radius: 50%”] {

width: 20px !important;

height: 20px !important;

line-height: 20px !important;

font-size: 0.7rem !important;

margin-right: 6px !important;

}

}

By

By

By

By