Table of Contents

- Executive Snapshot

- Introduction: The New Logic of Dealmaking

- Context: From Global Efficiency to Regional Resilience

- Key Insights: The New M&A Framework

- Drivers: Why the Shift Is Accelerating

- Counter-Narrative: The Risks of Over-Regionalization

- Opportunities: Where to Invest and Why

- Practical Guidance: Implementing the Framework

- Future Outlook: The Road Ahead

- Frequently Asked Questions

- Conclusion

Executive Snapshot

- Geopolitical volatility is redefining M&A priorities, shifting focus from cost optimization to supply chain resilience

- U.S. manufacturing assets are gaining traction as global buyers seek stability amid trade uncertainty

- Regionalization is accelerating, with companies prioritizing localized production and diversified supplier bases

- Digital systems are critical for enhancing visibility and control in fragmented supply networks

- Strategic acquisitions now target capabilities that mitigate disruption risks, not just reduce costs

Introduction: The New Logic of Dealmaking

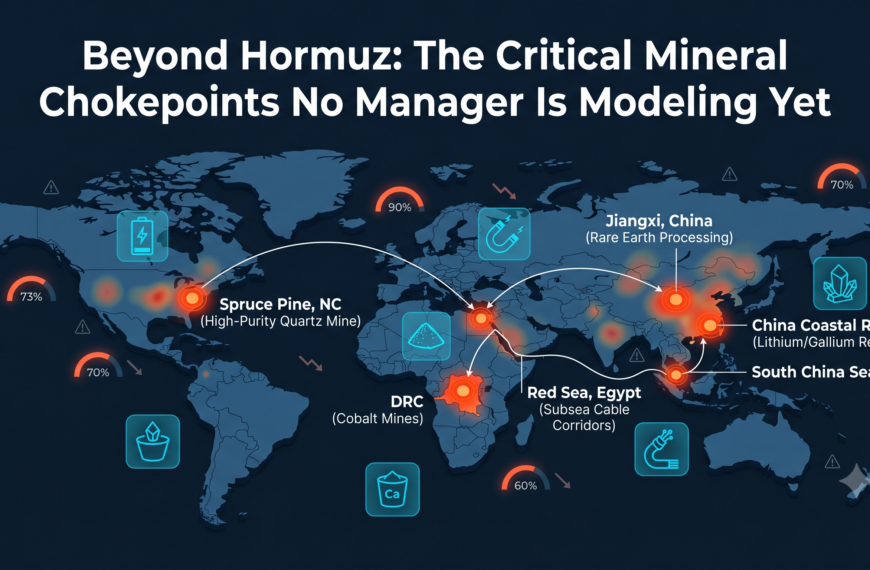

What drove this fundamental shift? Supply chain exposure. AI models flagged that critical cathode materials — including 73% of global cobalt from the DRC, most of which is processed through China — created single points of failure that export controls could exploit. The Chinese competitor wasn’t exposed to that bottleneck. The automaker was.

This is the new logic of dealmaking — and it is a perfect illustration of what I’ve been calling the Resilience Blind Spot. AI saw the vulnerability months before a crisis erupted, but only a board-level override — in the form of an acquisition — turned the warning into a hedge.

For decades, global supply chains were engineered around a singular objective: efficiency. Companies chased the lowest labor costs, exploited global scale, and optimized logistics to shave every penny. That model is being dismantled by tariffs, sanctions, export controls, and aggressive industrial policy. M&A strategies are no longer driven solely by financial metrics; they are driven by the imperative to insulate supply chains from disruption. This article unpacks how geopolitical risk is reshaping dealmaking and offers a framework for aligning M&A with long-term resilience.

Context: From Global Efficiency to Regional Resilience

The Shifting Paradigm

The traditional just-in-time supply chain model, which prized lean inventories and global sourcing, has proven acutely vulnerable to geopolitical shocks. Tariff volatility — most visibly the U.S.–China trade war — and sudden sanctions on Russian energy firms have exposed the fragility of extended global networks.

In 2025, global industrial, transport, and defense deals on Datasite surged 8% year over year, with an 18% increase in Q1 2026 compared to the same period in 2025. This acceleration signals a strategic pivot: companies are no longer waiting for policy clarity but are acting preemptively to secure supply chains.

The Rise of Regional Hubs

The shift toward regionalization is evident in cross-border investment flows. U.S. manufacturing assets are increasingly attractive to international buyers, driven by three factors:

- Tariff Mitigation: Proximity to end markets reduces exposure to import duties

- Regulatory Predictability: U.S. frameworks offer stability compared to opaque foreign policies

- Advanced Capabilities: Domestic production provides access to niche technologies like automation and industrial software, which are hard to replicate abroad

This trend is not limited to the U.S. Companies in Europe and Asia are also investing in regional hubs to shorten supply loops and reduce dependency on single-country suppliers.

Key Insights: The New M&A Framework

The 4 Pillars of Resilient Dealmaking

To navigate geopolitical risk, companies must adopt a structured approach to M&A. The following four pillars form the foundation of this new logic:

Pillar 1: Risk Mapping and Scenario Planning

Action: Identify critical nodes in the supply chain that are vulnerable to geopolitical shocks — semiconductor manufacturing in Taiwan, rare earth processing in China, quartz mining in Spruce Pine

Tool: Use geopolitical risk indices such as the Economist Intelligence Unit’s Global Risk Index to prioritize investments

Outcome: Allocate capital to regions with lower exposure to trade wars or sanctions

Pillar 2: Strategic Acquisition of Capabilities

Focus: Target assets that reduce bottlenecks or provide alternative sourcing options. For example, acquiring a logistics provider with regional distribution centers can stabilize throughput during disruptions

Example: The European automaker’s acquisition of a U.S. battery cell manufacturer to bypass tariffs and secure its EV supply chain

Pillar 3: Diversified Supplier Networks

Strategy: Move from single-source suppliers to a geographically diversified base. This includes both horizontal diversification and vertical integration

Data: A 2025 SupplyChainBrain survey found that companies with diversified supplier networks experienced up to 30% fewer production halts during geopolitical crises

Pillar 4: Digital Integration for Visibility

Technology: Invest in AI-driven supply-chain analytics and blockchain-based tracking to gain real-time visibility across tier-2 and tier-3 suppliers

Benefit: Enhanced visibility reduces lead times and enables agile decision-making when disruptions hit

“The old playbook of ‘find the best target and acquire it’ is dead. The new playbook is ‘build a resilient portfolio that performs across multiple geopolitical scenarios.’

Case Study: The Semiconductor Sector

The semiconductor industry exemplifies this shift. After the U.S.–China trade war, firms like Intel and TSMC accelerated investments in U.S. manufacturing. Intel’s $20 billion investment in Ohio fabrication plants was driven by the need to avoid Chinese tariffs and secure domestic supply chains — a move that reduced geopolitical risk and aligned with U.S. industrial policy incentives.

Drivers: Why the Shift Is Accelerating

Tariff Volatility as a Strategic Multiplier

Tariffs are no longer a one-time cost but a recurring variable. A 25% tariff on Chinese solar panels can increase production costs by 15 to 20% for U.S. manufacturers. This has prompted firms to acquire local suppliers or relocate production, even at the expense of short-term margins.

The Cost of Disruption

The financial impact of supply chain disruptions is staggering. A 2025 analysis by the World Bank estimated that supply chain shocks cost the global economy $1.5 trillion annually. That scale of loss has forced companies to prioritize resilience over pure cost cutting.

For instance, a 2026 automotive deal between a German OEM and a U.S. supplier was justified not by cost synergies but by the supplier’s ability to ensure uninterrupted component delivery during a potential Sino-American trade conflict.

Industrial Policy as a Catalyst

Governments are increasingly using industrial policy to shape supply chains. The U.S. CHIPS and Science Act provides tax incentives for semiconductor manufacturing. Companies are leveraging these policies to justify investments in domestic assets that also align with national security goals.

Counter-Narrative: The Risks of Over-Regionalization

While regionalization offers resilience, it is not without risks. Critics point to:

- Higher Costs: Localized production can increase unit costs by 10 to 15% due to higher labor and operational expenses

- Reduced Scale Economies: Fragmented supply chains may limit the ability to achieve global scale

- Over-Reliance on Domestic Markets: Companies may become vulnerable to domestic economic downturns or regulatory shifts

A 2025 analysis of European automotive firms found that those overly reliant on regional suppliers faced 12% lower profit margins compared to peers with more globally diversified networks. This underscores the need for a balanced approach: regionalization must be paired with strategic diversification, not a complete withdrawal from global markets.

Opportunities: Where to Invest and Why

Advanced Manufacturing Capabilities

Investing in regions with cutting-edge technologies — AI-driven robotics, additive manufacturing — can future-proof supply chains. A 2026 deal between a Japanese robotics firm and a U.S. manufacturer aimed to secure AI-powered automation capabilities, reducing dependency on Chinese suppliers.

Logistics and Last-Mile Solutions

Acquiring logistics partners with regional distribution networks stabilizes throughput. A 2025 acquisition by a Brazilian agribusiness of a U.S. cold-chain logistics provider ensured uninterrupted delivery of perishable goods amid trade tensions.

Niche Components and Critical Inputs

Securing suppliers of rare earth minerals, semiconductors, or pharmaceutical ingredients is critical. A 2026 deal between a European pharmaceutical firm and an Australian rare-earth miner highlights this trend — an acquisition aimed at avoiding Chinese export controls.

Practical Guidance: Implementing the Framework

Your 4-Step M&A Geopolitical Risk Checklist

✓ Step 1: Conduct a Geopolitical Risk Audit

Map all suppliers, production sites, and logistics partners against geopolitical risk indices. Use platforms like S&P Global Market Intelligence or the Deloitte Geopolitical Risk Index. Identify high-risk nodes and prioritize investments to mitigate exposure.

✓ Step 2: Align M&A with Strategic Objectives

If your risk audit flags over-reliance on Chinese electronics, target acquisitions in Vietnam or India to diversify sourcing. Ensure that 70% of critical components come from diversified suppliers.

✓ Step 3: Leverage Digital Twins for Scenario Testing

Deploy digital twins of supply chains to simulate disruptions — trade war, natural disaster. Identify vulnerabilities and test the impact of different M&A strategies before committing capital.

✓ Step 4: Integrate ESG and Regulatory Compliance

Acquire companies with strong ESG practices to avoid regulatory penalties and reputational damage. A 2026 acquisition by a European retailer of a U.S. logistics firm with carbon-neutral operations is a live example.

Future Outlook: The Road Ahead

The next 5 to 10 years will see further fragmentation of global supply chains. Emerging technologies like AI and blockchain will enable more agile, decentralized networks. However, the balance between resilience and efficiency will remain a key challenge. Companies that successfully integrate geopolitical risk into their M&A strategies will dominate; those clinging to outdated models risk obsolescence.

Frequently Asked Questions

How do geopolitical risks specifically influence M&A valuations?

Geopolitical risks increase the perceived cost of disruption, leading to higher premiums for assets that provide resilience. According to a 2025 Deloitte survey of corporate acquirers, a supplier with diversified production bases can command a 15 to 20% valuation premium over a single-country-focused competitor — a premium buyers are increasingly willing to pay.

What are the most vulnerable sectors to geopolitical shocks?

Sectors reliant on concentrated sourcing — semiconductors, pharmaceuticals, rare earths — are most vulnerable. These industries accounted for roughly 60% of global supply chain disruptions in 2025, according to SupplyChainBrain.

Can digital tools fully mitigate geopolitical risks in supply chains?

No. Digital tools dramatically enhance visibility and speed of response, but they cannot eliminate risks like sanctions or trade wars. As my earlier article on the six critical mineral chokepoints showed, even the best AI monitoring cannot prevent a supply cut — it can only buy you time to react.

How do U.S. industrial policies affect M&A in supply chains?

U.S. policies like the CHIPS Act provide tax incentives for domestic investments, making U.S. assets more attractive. Datasite reported a 35% increase in cross-border deals targeting U.S. manufacturing in 2026, driven in part by these policy tailwinds.

What role do ESG factors play in M&A decisions related to geopolitical risk?

ESG compliance reduces regulatory and reputational risks. McKinsey’s 2025 research indicates that companies acquiring ESG-compliant suppliers see 20% lower litigation costs and 15% higher stakeholder trust scores.

Conclusion

The geopolitical landscape has rewritten the rules of M&A in supply chains. Companies that continue to view deals as cost-reduction tools will lose. Companies that view deals as resilience investments will win. The 4-Pillar framework outlined here is not optional — it is the new baseline. In this era, resilience is not a luxury. It is the foundation of competitive advantage.

For the deeper conceptual architecture behind this shift — the gap between what AI predicts and what institutions act upon — revisit the Predictability Paradox and its companion piece on the Resilience Blind Spot.

This article is part of the ILMI Initiative’s ongoing analysis of how AI, geopolitics, and supply-chain risk are reshaping strategy and decision-making. For the full series, visit the World Affairs category.

Published by ILMI Initiative (International Liquidity and Market Intelligence Initiative) | Research on global market risks and supply chain vulnerabilities

By

By

By

By